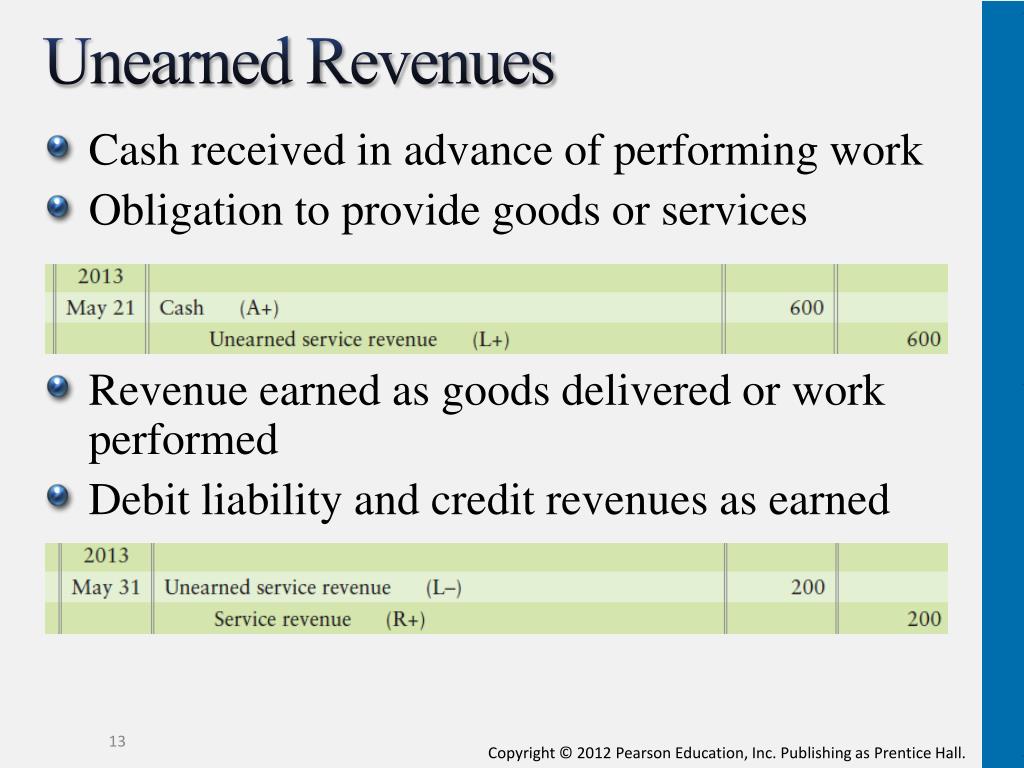

Are built property has actually given a decreased-cost replacement for antique site-established property for decades. Needed zero-maintenance, was affordable, and can be designed to match your book needs. In place of to find a classic single-nearest and dearest possessions, you may opt for just one-large are produced home.

Capital their unmarried-large are manufactured household will differ from to acquire a traditional household. That is because loan providers categorize are manufactured home (MH) once the private possessions instead of a house. Its terms to possess MH are also modifying as demands to have this type of properties continue ascending.

The condition of the newest MH you are searching to purchase can impact their capital. Investing in good-top quality single-wider MH will bring you a home loan with advantageous cost.

Within book, i break apart the brand new five types of financing (FHA, Va, USDA, and you can conventional) which you can use purchasing an individual-broad MH:

Money a single-Wide MH that have an enthusiastic FHA Loan

You need an enthusiastic FHA mortgage to finance just one-broad MH, given our home are taxable as the real estate. The house ought to be permanently repaired in order to your state-acknowledged foundation.

Types of FHA MH Financing

You can simply take three version of FHA fund to invest in a good single-greater MH. You may submit an application for a created mortgage purchasing a beneficial new/used MH, as well as basis will be based with the. A made household lot financing try specifically designed to purchase the foundation of an enthusiastic MH.

The 3rd form of FHA MH loan is the are built domestic buy loan. It can be utilized buying a keen MH only rather than base.

To possess FHA are created mortgage brokers, you should buy a concept I or a title II. A concept We financing helps you money much or both MH and parcel. Referring that have a repayment term all the way to two decades into the possessions and parcel and you will 15 years to your lot just.

Loan limitations to your domestic and base stand in the $92,904 and you will $69,678, and you may $23,226 into family and you will foundation, correspondingly.

A name II FHA loan would-be best whether your solitary-wide MH try an individual-family home property. The borrowed funds also offers good forty-12 months funding name.

FHA MH Mortgage Conditions

Brand new personal loans Utah unmarried-wide MH’s framework need see HUD’s MHCSS requirements to get eligible to have a keen FHA MH mortgage. It ought to along with see FHA’s livability and you can shelter conditions and be appraised because of the a keen FHA-accredited appraiser.

The newest borrowing from the bank conditions is a good 3.5 per cent minimum advance payment and you can an effective 530 credit rating. The debt-to-money ratio ought to be 50 percent or smaller to meet the requirements.

Interest levels

Assume certain loan providers so you’re able to charges large-interest rates for a keen MH loan for several reasons. The fresh new higher-interest levels ounts, that have a small profit margin.

It is also popular to own a lender so you’re able to costs a top-rate of interest if your MH house appears glamorous based on its possible selling worthy of.

Rates differ with your credit history and you can get, DTI, and you can down payment. You can aquire an aggressive interest to your solitary-wide MH which have lower costs, advanced borrowing, and you can substantial discounts.

Try Insurance policies Necessary?

In place of antique mortgage loans, FHA mortgage brokers do not require one to possess Private Home loan Insurance policies (PMI). Instead, needed one to shell out a paid and you will upfront mortgage insurance policies superior.

The mortgage may require an effective MIP to have a varied go out mainly based for the mortgage fine print. FHA-backed mortgage brokers rely on MIPs to shield by themselves facing higher-risk consumers.

Financing a single-Greater MH as a result of a great Virtual assistant Financing

Military professionals and you can pros are able to use its Va loan advantages to fund an individual-large MH. Although not, the fresh new Va mortgage system classifies each other are formulated and cellular home since the same thing.