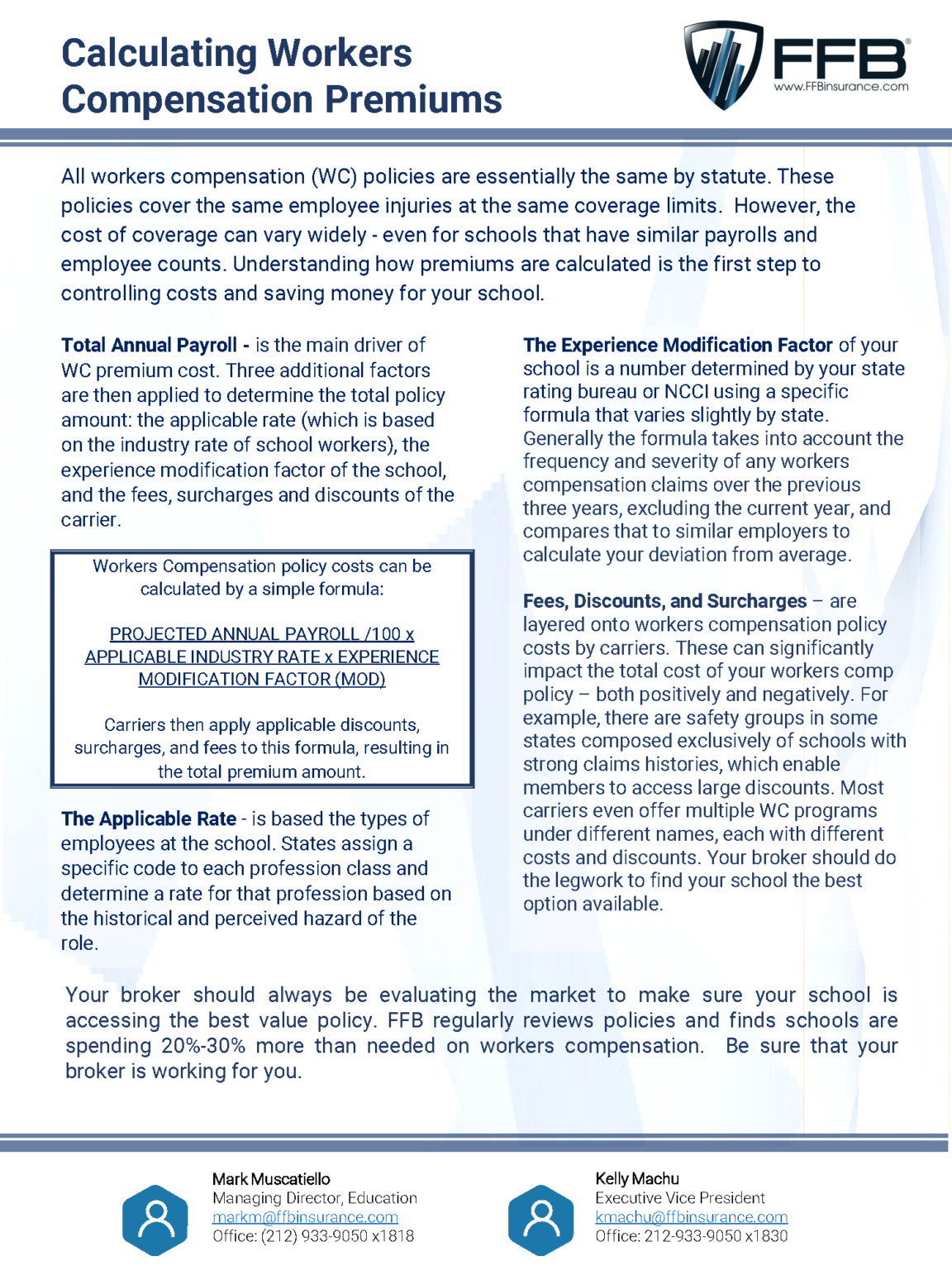

Loan providers like to see that you could create month-to-month mortgage repayments and will not default into financing. For the, they’ve been looking economic stability. This might be shown with a decent credit history, offers, funding membership and you can numerous income streams.

Whenever you are mind-functioning, your work history getting a home loan may well not meet extremely lenders. Instead, you could highlight other money avenues, for example self-employed really works, leasing money and you will financial support income, exhibiting full economic balance.

cuatro. Improve your Deals

A substantial checking account can help have demostrated obligation and you will fiscal duty, mitigating the possibility of contradictory work. While there is absolutely no secret count, if you can reveal good deals, comparable to that 3 years or even more from mortgage repayments, it can be better to safe a home loan having less than one year from functions background.

When underwriters see business history to own home financing, a position holes try warning flags, however with planning, you could potentially browse all of them. Given that possible lenders might inquire about holes on your a career records, it’s best to has a coherent reason ready.

If you were underemployed on account of illness, burns and other factors, anticipate to offer files to support their story. If perhaps you were volunteering, taking a-year abroad or any other interest, become it on the work record to help fill in any holes – and assure all of them that you’re not think that again.

6. Bring an effective Credit score

One to metric finance companies consider whenever comparing home loan software is actually a good borrower’s credit history. And make for the-date money and you may minimizing their credit utilization can enhance your get and increase the possibilities of recognition. Opt for a credit score out of 740 or more than to boost your odds of acceptance.

Keep in mind that you can access your credit report at annualcreditreport so you can look for for which you currently sit and to ensure that most of the information on the financing statement is correct. Contemplate using a lease revealing team so you can breakdown of-time leasing and you may tools repayments to improve your credit rating reduced. To-be a 3rd party associate towards the an effective pal’s or friends member’s borrowing from the bank cards can also boost your credit history – as long as its credit score or credit rating was drastically greatest.

seven. Consult a mortgage broker

Professional lenders can also be connect you that have a suitable bank dependent in your financial situation. They have relationships with several lenders, which could make the procedure of bringing a mortgage a lot more available and you may smoother. They will certainly do some of your own research and you will behave as an enthusiastic advocate in your stead regarding the mortgage software process, also without many years on your own career to greatly help rating property mortgage.

8. Be ready to Render A lot more Paperwork

When you’re asked for more papers in financial application process, think it over a good signal. He could be happy to examine the job but could request bank statements loans New London and other financial comments, tax returns and a career records to exhibit eligibility. To cease waits or denials, be sure things are managed just before your application.

nine. Think Co-Individuals

When your work history might possibly be top, while can’t have demostrated a strong economic instance with high credit rating, larger advance payment and you will offers, believe launching a good co-candidate that have a far more uniform employment checklist. The brand new co-applicant doesn’t need to end up being a co-holder of the home, merely a beneficial co-signer into the financial to help with the application and help you qualify.

ten. Dont Quit

Even though you have less age in a career, a mortgage isn’t really out of reach. Show patience and you can persistent, and you may explore the options very carefully to find the financial you want. A mortgage broker otherwise co-signer is also discover gates.